Here are some of the key drivers:

1. Low interest rates. Before the rate hikes began in May 2022, the cash rate sat at just 0.10%. Cheap borrowing costs made mortgages more accessible, fuelling buyer demand and pushing up prices.

2. Population growth. Rising immigration and natural population increases added pressure to housing demand – particularly in the capital cities where most new arrivals tend to settle.

3. Limited housing supply. While demand surged, supply lagged behind. A slowdown in building approvals and rising construction costs contributed to a growing housing shortfall.

4. Wage growth and low unemployment. Low unemployment and steady wage growth gave many buyers the confidence – and borrowing power – to enter the market.

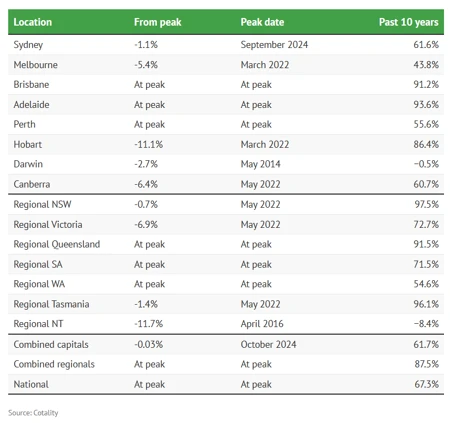

Of course, such rapid growth has come at a cost. Affordability has taken a hit, with property prices outpacing incomes and mortgage repayments consuming a larger share of household budgets. First home buyers, in particular, are feeling the squeeze.

So what’s next?

Most analysts expect home values to keep rising, but at a slower pace. Affordability constraints will play a bigger role, although further interest rate cuts and government support – such as low-deposit loans and housing supply initiatives – could help keep the market moving.

If you’re in the market to buy a home and want an idea of the size of home loan you qualify for, our mortgage calculator can help you determine your borrowing capacity. Click here to complete a short 60-second form.